The All-Inclusive Overview To Employing An Estate Planning Attorney: Wills, Counts On, Property Security, And Legacy Planning |

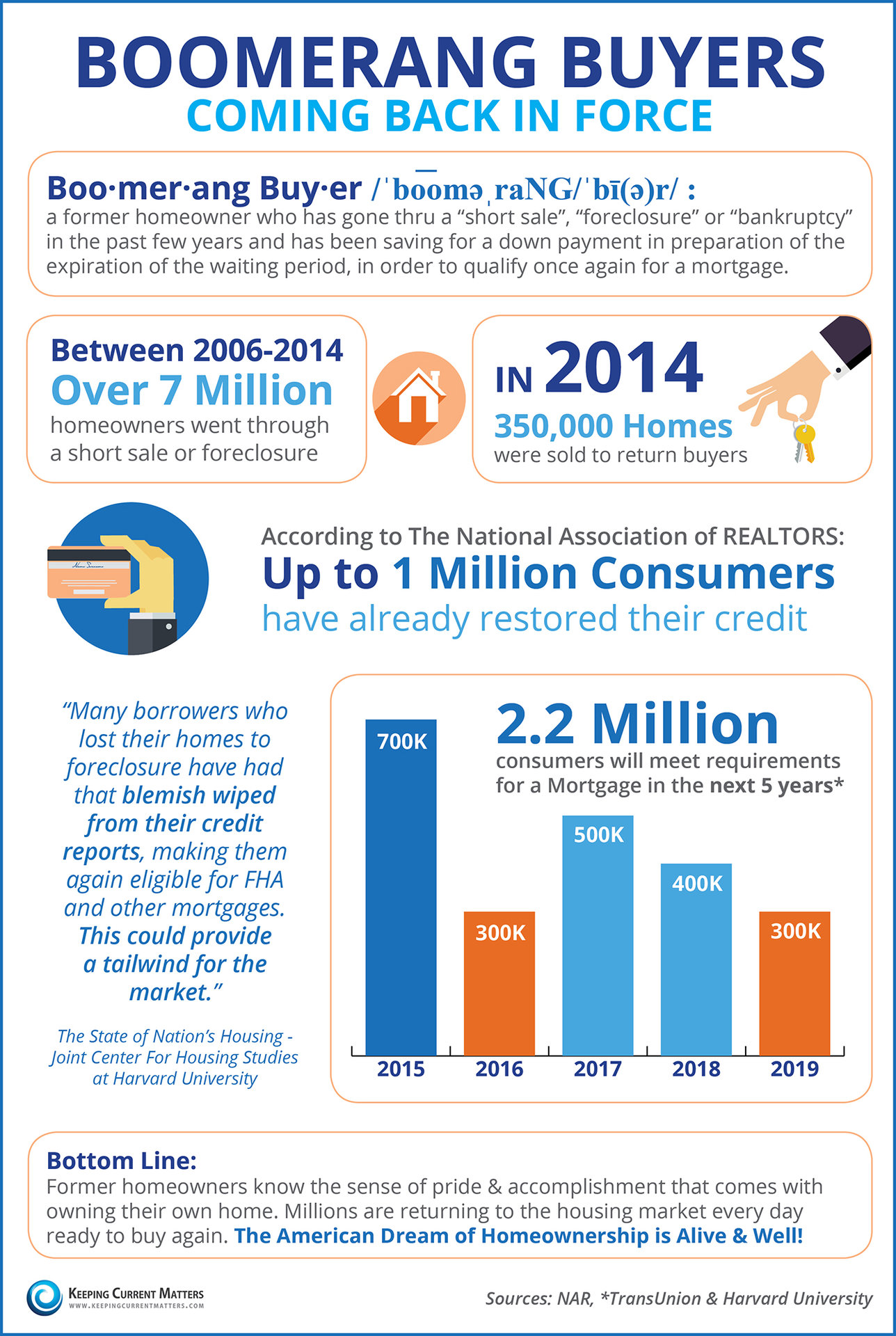

https://www.realtor.com/advice/buy/bidding-war-mistakes-homebuyers-are-making-today/ Composed By-Dahlgaard Svensson

When it concerns protecting your heritage, employing the appropriate estate Planning attorney is important. You require someone who recognizes your special objectives for possession distribution and defense. With a lot of choices out there, exactly how do you find the appropriate fit? By carefully assessing your requirements and reviewing potential prospects, you can make an enlightened choice. However what specific inquiries should you ask during assessments to ensure you're on the ideal course?

The Probate Process Demystified: How A Probate Lawyer Facilitates Efficient Estate Resolution |

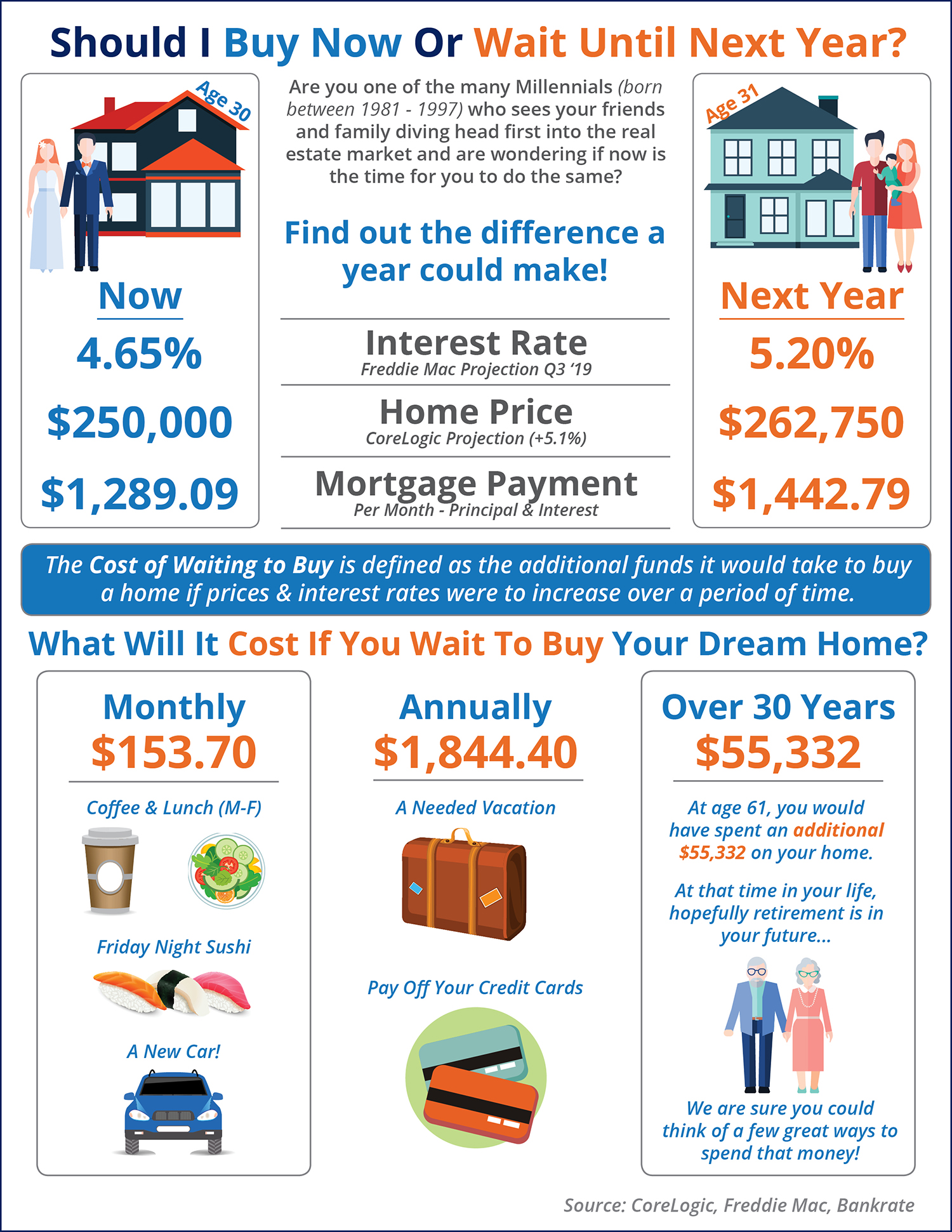

https://www.bankrate.com/real-estate/should-i-buy-a-house-now-or-wait/ Developed By-Carlsen Poe

When a liked one passes, navigating the probate procedure can feel frustrating. You might locate on your own dealing with complicated lawful requirements and emotional obstacles as you attempt to settle their estate. Comprehending how a probate attorney can aid you is crucial in making this process much more manageable. Their expertise can assist you avoid common challenges and make certain whatever runs smoothly. However what https://dantepkgau.blog-mall.com/43178650/identify...ing-economic-safety-is-crucial can you expect, and just how can an attorney assistance?

Estate Planning Checklist: Exactly How An Estate Planning Attorney Can Assist You Avoid Costly Lawful Errors |

Short Article Composed By-Churchill Banks

When it pertains to estate Planning, you might think it's as easy as drafting a will. Nonetheless, the reality is far more complicated, and a small oversight can result in pricey lawful disputes. An estate Planning lawyer can lead you via essential files and customize them to your details scenarios. Comprehending exactly how they can aid you stay clear of these pitfalls is crucial, especially when thinking about the ramifications for your enjoyed ones. What should https://chicagoagentmagazine.com/2022/07/04/grigory-greg-pekarsky/ understand next?

The Comprehensive Handbook For Picking An Estate Planning Lawyer: Wills, Counts On, Property Safeguarding, And Legacy Method |

Web Content Written By-Bank Holbrook

When it pertains to securing your heritage, hiring the appropriate estate Planning lawyer is important. You need someone that comprehends your special goals for property circulation and protection. With numerous choices available, exactly how do you find the right fit? By thoroughly assessing your demands and examining prospective prospects, you can make an informed selection. But what specific inquiries should you ask during examinations to ensure you get on the right course?

Trusts Vs Wills: An Estate Planning Lawyer Reviews Which Course Is Most Proper For Your Monetary Interests |

Written By-Braswell Huber

When planning your estate, you may ask yourself whether a depend on or a will is the far better fit for your monetary objectives. Each choice has its very own benefits, and the right choice usually depends on your distinct conditions. Depends on can give more control and privacy, while wills offer simplicity for uncomplicated estates. Yet just how do you recognize which path to take? Allow's check out the subtleties that might significantly impact your estate Planning choices.

The All-Inclusive Overview To Working With An Estate Planning Attorney: Wills, Counts On, Asset Security, And Legacy Planning |

Web Content Writer-Basse Jonsson

When it comes to protecting your tradition, hiring the ideal estate Planning lawyer is important. You require a person that understands your unique objectives for property distribution and security. With so many options out there, how do you locate the right fit? By meticulously analyzing your needs and examining potential candidates, you can make an educated choice. But what particular inquiries should you ask throughout appointments to ensure you get on the ideal path?

What Solutions Does An Estate Planning Lawyer Supply? Essential Truths To Testimonial Prior To Crafting Your Estate Strategy |

Article By-Johnson Ibrahim

When you think of safeguarding your future, an estate Planning lawyer is crucial. https://www.tallahassee.com/press-release/story/86...rd-deeds-in-melbourne-florida/ guide you via the procedure of producing a strategy that shows your dreams, from drafting wills to developing depends on. You may question what details solutions they use and how to select the appropriate one for your requirements. Recognizing these details can make a substantial difference in your estate planning journey. So, what should you think about before making that selection?

Comparing Estate Planning Lawyer And Probate Lawyer: Insights On When To Seek Advice From Each |

Web Content Writer-MacGregor Peele

When it involves managing your possessions and guaranteeing your dreams are recognized, recognizing the roles of an estate Planning attorney and a probate attorney is vital. You may believe they offer similar purposes, but their features are quite unique. Recognizing when to consult each specialist can streamline the frequently complex globe of estate monitoring. But how do you identify which one you need at different phases of your life? Let's explore their special roles.

Escaping Probate: The Benefits Of Involving An Estate Planning Attorney To Guard Your Estate And Minimize Time For Your Household |

Team Writer-MacMillan Hewitt

When it comes to shielding your estate, staying clear of probate is crucial. It can save your family members time and reduce anxiety throughout an already tough duration. An estate Planning attorney can guide you with this process, ensuring your desires are honored and your possessions are dispersed successfully. However what techniques can they apply to improve your estate strategy? Comprehending these techniques can make a substantial distinction for your liked ones.

What Are The Consequences Of Diing Without A Will? The Significance Of Employing An Estate Planning Attorney. |

Write-Up Developed By-Warren Parrish

If you pass away without a will, you're leaving your enjoyed ones to navigate a complex legal puzzle. State legislations will dictate exactly how your possessions are distributed, usually prioritizing spouses and kids while potentially omitting others you may intend to include. This can lead to disagreements that include emotional pressure throughout a currently tough time. Comprehending these effects is critical, which's where an estate Planning lawyer is available in. What do you need to recognize next?

Get Understandings On The Costs Of A Real Estate Closing Lawyer And Find The Services That Can Make Or Break Your Purchase. What Should You Expect? |

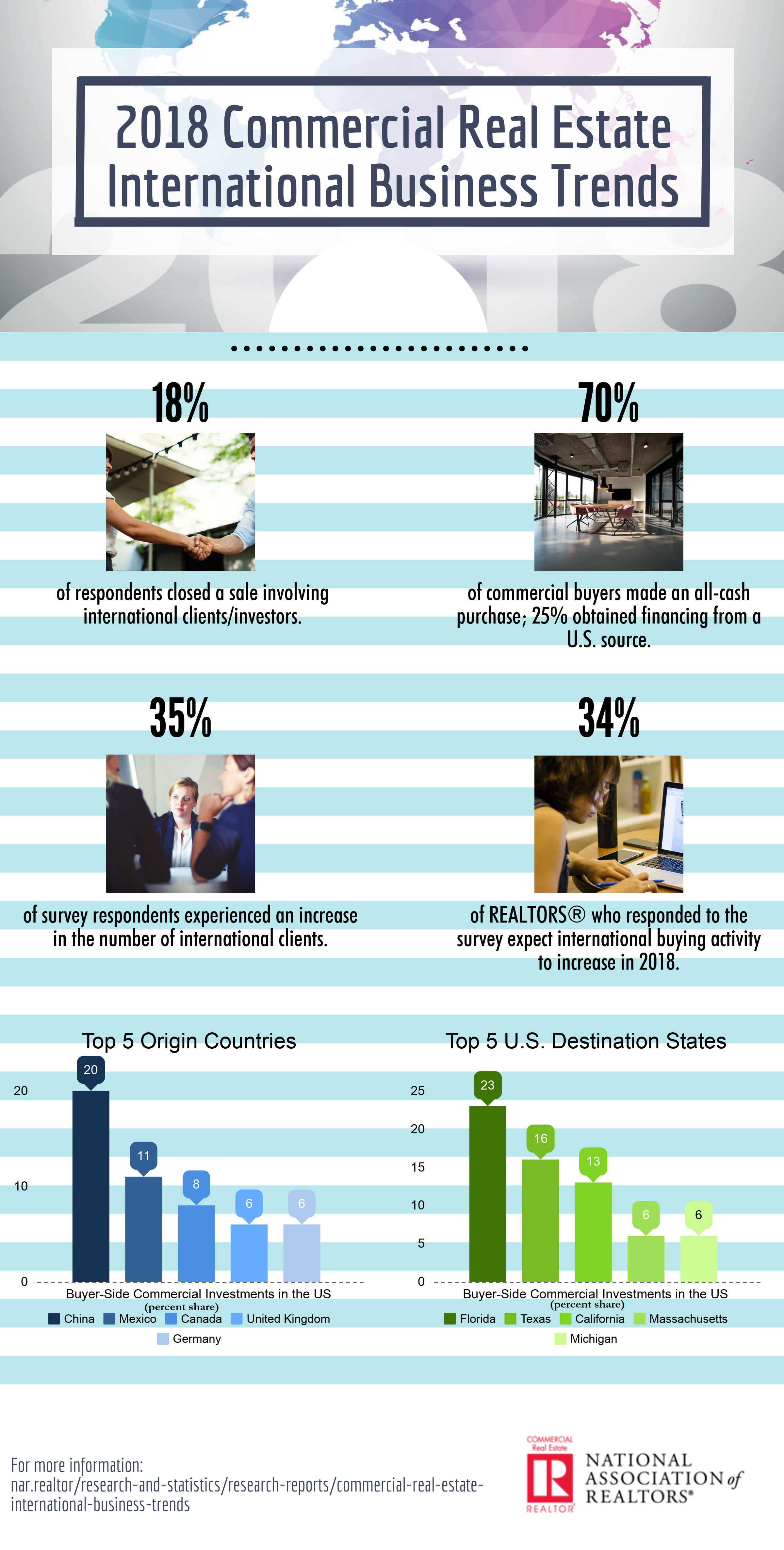

https://themortgagereports.com/91167/is-buying-a-house-a-waste-of-money-in-2022 Develop By-Leon Axelsen

When you're browsing the intricacies of a real estate purchase, comprehending the costs connected with a closing attorney is important. Generally, you can expect to pay between $500 and $1,500, depending upon your place and the bargain's ins and outs. But just what affects these charges, and what solutions do these attorneys supply to guarantee a smooth closing? Let's explore the information that can influence your spending plan and experience in this important process.

A Clear Understanding Of Closing And Title Attorneys Is Important For Effective Real Estate Purchases, But What Crucial Distinctions Should You Be Aware Of? |

Content Writer-Battle Day

When you're navigating real estate transactions, having the ideal lawful support can make all the difference. A closing attorney deals with the complexities of the closing procedure, while a title lawyer safeguards your building legal rights. Recognizing their duties is necessary to make sure a smooth experience. However what exactly establishes these 2 specialists apart, and just how do they collaborate to secure your interests? Let's discover the crucial aspects you need to think about.

Discover Why Working With An Estate Planning Attorney Is Vital For Senior Citizens To Safeguard Their Dreams And Possessions-- Your Assurance Depends On It |

Published By-Randrup Mcfarland

As you go into retirement, estate Planning becomes more important than ever. It's not almost dispersing possessions; it's about guaranteeing your healthcare desires are recognized and your enjoyed ones are looked after. Hiring an estate Planning lawyer can simplify this process, leading you with legal intricacies and helping you produce a plan tailored to your requirements. However just what should you take into consideration when picking the ideal lawyer for your circumstance?

Just What Vital Questions Should You Ask An Estate Planning Attorney? Discover Vital Insights To Ensure Your Future Is Protected |

Short Article Created By-Barker Vendelbo

When you're considering hiring an estate Planning attorney for your will or trust, asking the ideal concerns is vital. You intend to ensure they have the experience and approach that fits your needs. It's not just about composing papers; it has to do with comprehending your special scenario and future modifications. Curious regarding what you should ask? Allow's discover the key questions that can assist you in making an educated decision.

Exactly How Can Reliable Estate Planning Methods Protect Your Family Members'S Wide Range? Discover Professional Insights That Might Transform Your Heritage And Guarantee Assurance |

Write- how high net worth families avoid estate taxes Created By-Childers Hanley

When it pertains to securing your family's future, recognizing estate Planning techniques is critical. You could wonder whether a will or depend on is the best suitable for your situation. Navigating the intricacies of tax ramifications and guardianship can really feel frustrating. However, having the right assistance can streamline the procedure and protect your legacy. Let's check out exactly how these techniques can work together to guarantee your desires are honored while lessening prospective disputes.

What To Try To Find In An Estate Planning Attorney: Specialist Tips For Smart Decision-Making |

Short Article By-Connor Tonnesen

Selecting the right estate Planning attorney can feel overwhelming, yet it's critical for safeguarding your assets and recognizing your desires. You require somebody with the ideal experience and an interaction design that resonates with you. Individual values likewise play a significant function in this decision. So, what certain qualifications should you prioritize, and just how can you guarantee your attorney recognizes your unique needs? Allow's explore https://writeablog.net/vicenta2brett/secure-your-a...hts-on-what-an-estate-planning .

Encountering Prospective Legal And Monetary Threats? Discover Just How An Estate Planning Attorney Can Secure Your Assets And Ensure Your Tradition Stays Undamaged |

Short Article Author-Frank Oddershede

When you consider protecting your properties, an estate Planning lawyer becomes important. They craft tailored strategies to secure your wealth from lawful and monetary dangers. With tools like revocable living counts on, they assist you avoid probate and defend against financial institution insurance claims. Yet that's simply the beginning. There are much deeper layers to consider, specifically when it concerns tax obligations and family dynamics. Recognizing these subtleties can make all the distinction in securing your legacy.

Planning Your Estate? Discover Whether Working With A Lawyer Is Worth The Investment And What Long-Term Advantages You Could Be Missing Out On |

Created By-Skytte Patton

When taking into consideration whether to employ an estate Planning attorney, you could question if the expenses warrant the prospective advantages. While the fees can appear complicated, the lasting advantages commonly surpass them. A professional can assist guarantee your desires are recognized, reduce taxes, and protect your properties. However just how do you evaluate these aspects? Allow's explore the costs involved and the vital advantages you could not have considered.

Looking To Safeguard Your Household'S Future? Discover How A Skilled Estate Planning Attorney Can Streamline Your Journey And Safeguard Your Dreams Efficiently |

get more info -Kring Bray

When it comes to protecting your family members's future, estate Planning is essential. You might assume you can manage it on your own, yet the intricacies of wills, trust funds, and asset circulation can promptly end up being overwhelming. That's where a skilled estate Planning attorney can be found in. They not only simplify the procedure but likewise ensure your dreams are plainly verbalized. Interested about the details means they can help you?

Selecting The Appropriate Estate Planning Lawyer Is Essential; Uncover Key Qualifications That Ensure Your One-Of-A-Kind Needs Are Satisfied And Your Dreams Honored |

read review By-Connor Timm

Selecting the appropriate estate Planning lawyer can really feel frustrating, however it's essential for shielding your properties and honoring your dreams. You need a person with the ideal experience and a communication style that resonates with you. Individual worths likewise play a significant duty in this choice. So, what specific certifications should you focus on, and just how can you ensure your attorney recognizes your special demands? Let's explore these vital factors.

Be Prepared To Safeguard Your Family'S Economic Future By Uncovering Crucial Ideas For Picking The Excellent Estate Planning Lawyer For Your Special Demands |

Posted By-Sexton Skovgaard

When it comes to securing your family's economic future, picking the ideal estate Planning lawyer is critical. You require a person who not just recognizes the ins and outs of estate regulation however additionally aligns with your family members's distinct demands. As you begin this crucial trip, it's vital to know what credentials to prioritize and exactly how to determine a lawyer's track record. So, what should you try to find in a possible prospect? Allow's discover the vital elements to take into consideration.

Just How An Estate Planning Attorney Protects Your Assets From Legal And Financial Threats |

Uploaded By-Frank Roman

When you think about securing your assets, an estate Planning lawyer comes to be vital. They craft customized techniques to protect your wide range from legal and financial dangers. With tools like revocable living trust funds, they help you avoid probate and guard against creditor claims. However that's just the beginning. There are deeper layers to take into consideration, especially when it comes to tax liabilities and family members characteristics. Recognizing these nuances can make all the distinction in protecting your legacy.